ANALYSIS: Adobe (ADBE)

Responsible Enterprise AI + GEO Optionality at Decade Lows

I generally don’t go for ‘pure play’ tech stocks but here we have a company with a fortress balance sheet, gushing free-cash flow and is set to benefit from AI adoption. Despite this being a $130bn market cap company with a brand everyone is familiar with - no one talks about them.

When most investors think about AI winners, they picture foundation model companies or flashy startups. They’re missing Adobe, a company quietly building one of the most defensible positions in enterprise AI while trading at decade-low valuations.

Adobe’s next decade of value creation will likely mirror its last: converting adoption into monetization through bundled value and workflow lock-in. The Company is uniquely positioned to capture enterprise AI spend by solving the critical IP and legal risks that prevent broader adoption, while leveraging its unmatched distribution network to monetize AI at minimal customer acquisition cost.

Finally, I think Adobe is positioning itself to be a heavyweight in the nascent GEO (Generative AI Engine Optimization) space, an area I think is going to become increasingly important to DTC, ecommerce and digital media businesses.

This is a Company which has an incredibly stable recurring revenue stream at high, stable margins. Assuming no multiple expansion, revenue growth and buybacks alone should get you to a 17% IRR. Considering, Adobe is trading at a decade low, multiple expansion isn’t out of the question.

Special shoutout to Philoinvestor, whose Netflix post which highlighted distribution has stuck with me ever since reading it (a rarity!) and Citrini who recently spoke about the enterprise AI ‘losers’ who may be gearing for a big reversal.

Business Overview

Adobe’s value creation over the past decade came from three core strategies: converting perpetual licenses to subscriptions, expanding average revenue per user through bundled value, and driving exceptionally low churn through workflow lock-in. The company now operates across three primary segments.

Creative Cloud remains the major business driver. Adobe commands an estimated 32 million Photoshop users and maintains a dominant position in creative software. Adobe itself estimates it controls 20% of the Creative software TAM, concentration you don’t see every day. The Company recently moved its all-in AI video editor to public beta, with early reviews putting it ahead of OpenAI and Google, who offer image and audio generation but not comprehensive AI-native video editing packages.

Document Cloud serves 650 million monthly active users for Acrobat. With 3 trillion PDFs in existence globally and over 400 billion documents opened in Acrobat annually, this represents one of the few products comparable to Microsoft Office in terms consumer penetration.

Experience Cloud serves 12,000 enterprise customers, including 87% of the Fortune 100 and 74% of the Fortune 500. This segment is probably the least-known to the average person on the street but here too, Adobe shows dominance: Gartner’s Magic Quadrant lists Adobe’s Experience Platform as a Leader in digital experience platforms. Experience Cloud focuses on marketing campaign management and data analytics. The segment also provides optionality through GEO exposure via LLM Optimizer and the recent SEMRush acquisition.

Adobe’s total addressable market stood at $205 billion in 2024 and is projected to reach $293 billion by 2027, representing a 14% CAGR. While growing slower than the overall market, Adobe already commands significant market share: approximately 8% of the Document TAM, 4% of Content Management TAM, and 20% of Creative TAM (the primary business driver).

Investment Thesis

Enterprise AI Adoption’s Pain Point: Security and Legal Risk

A 2025 study revealed that most enterprises admit they are not prepared for AI security risks, citing it as a major concern. OECD surveys show significant gaps between AI adoption intent and actual implementation due to security and privavy concerns. High-profile legal actions are shaping the competitive landscape. Midjourney, which has taken a laissez faire approach to image generation and IP has been sued by Anderson, Disney, Universal, and Warner Bros for copyright infringement.

This creates a fundamental barrier to enterprise AI adoption. Companies want the productivity gains but cannot stomach the legal exposure.

Adobe’s Triple-Layered Protection

Adobe addresses this pain point through three defensive layers that competitors cannot easily replicate.

Layer 1: Blanket Indemnification

Adobe, alongside Microsoft and Google, offers blanket indemnification for any output enterprise users produce. This protection creates a barrier to entry that only large-scale, highly profitable companies can afford to provide (such as Microsoft and Google). Smaller AI startups do not have the financials to offer similar incentives.

Layer 2: Licensed Training Data

Adobe trains exclusively on licensed data from Adobe Stock, strengthening its position with privacy-conscious customers. Adobe Stock contains hundreds of millions of images, videos, vectors, and 3D assets accumulated over decades. Contributors are paid, providing clear contractual rights for derivative model training.

The cost to replicate this moat is likely too large for any company to try: building a contributor marketplace, establishing reputation, paying thousands or millions of users per download, and providing indemnification. This moat took Adobe decades to build.

Layer 3: Firefly Foundry (Custom Enterprise Models)

Firefly Foundry trains custom models exclusively on enterprise customer data, addressing niche use cases where off-the-shelf large language models fall short. This guarantees privacy and data protection while eliminating in-house model building operating expenses.

More importantly, it creates massive switching costs. As one past user explained: “The Firefly Foundry strategy is clever because it sidesteps the commoditization risk that’s hitting most gen-AI tools. When enterprises train on their own brand assets and guidelines, they’re basically locking themselves deeper into the Adobe ecosystem. I saw this up close when a marketing team I worked with spent six months building custom models and now switching costs are enormous.”

The strategy also creates significant upsell opportunities. As per management: one media client expanded from $10 million to approximately $17 million in annual recurring revenue by combining traditional creative products with Firefly Services and Foundry.

Competitive Dynamics

While AI image generators may serve as ideation tools (Midjourney and Canva for concept development), enterprises need legally defensible, commercially viable final assets. Most professional designers may use other tools to quickly scale up ideas, the asset itself will still be done in Photoshop. Adobe is positioning Firefly as the safe choice for production-ready content, while competitors remain confined to the inspiration phase.

According to Adobe’s blog in October 2025, 86% of creatives use generative AI in workflows, yet 45% say they will never trust generative AI to produce final assets. Human post-production and editing remain critical.

Adobe’s brand trust reinforces this positioning. The company ranks #2 on Newsweek’s 2025 America’s Most Trusted Businesses and #20 on Interbrand’s Best Global Brands with a $41 billion brand valuation, ahead of Hermès, IBM, and Netflix.

Adobe’s Distribution Network: The Ultimate Competitive Advantage

If product is king (OpenAI), then distribution is god (h/t Philoinvestor). Adobe possesses one of the deepest distribution networks in enterprise software.

Consumer and Professional Reach

Acrobat serves 650 million monthly active users across free and paid tiers. It’s the only product comparable to Microsoft Office (approximately 1 billion users) in consumer penetration. Free AI features shipped into Acrobat serve as an on-ramp for premium AI features, creating another monetization vector for free users.

Creative Cloud serves 37 million users. Adobe Experience serves 12,000 enterprise customers, representing 87% of the Fortune 100 and 74% of the Fortune 500. These are deep distribution networks running across multiple markets and client-types.

Microsoft Copilot provides a case study: it became one of the most used chatbots primarily due to Microsoft’s distribution network, despite modest conversion rates.

Zero Marginal Customer Acquisition Cost for AI Products

Adobe can ship AI products pre-bundled or deploy remote updates to its entire installed base at zero marginal customer acquisition cost. There is no need to build sales channels from scratch as the sales funnels and relationships are all pre-existing. In the Creative segment, most users are already paid subscribers, which are significantly more receptive to AI feature upsells.

The proof point: Adobe’s AI generative fill feature in Photoshop achieved 10x faster adoption than average Creative features, according to the company’s 2023 Investor Day Deck.

Financially Underwriting AI Investment

Inference training requires upfront costs. Monetization only comes later once a critical mass of subscriber users has been acquired. Upstarts need to fund inference training through venture capital or debt markets. Adobe’s $25 billion subscription annual recurring revenue base provides highly predictable cash flow to underwrite inference costs with financial discipline without risking dilution or turning their balance sheet upside down (Cough, cough, Oracle).

The result: gross margins haven’t changed post-Firefly roll out. This margin management came about from zero incremental sales cost and training costs spread across millions of paying users.

The Walled Garden Thesis

AI models will eventually converge in quality and commoditize. Value will accrue to walled gardens integrated into pre-existing ecosystems and workflows. Think Microsoft Office versus alternative productivity tools, or Salesforce versus standalone CRMs.

Native AI within enterprise ecosystems will retain users through seamlessness and workflow integration. General AIs will face pricing compression as they get commoditized. Workflow-embedded AIs should retain pricing power through upsell opportunities in pre-existing bundles. Privacy and regulatory benefits provide additional defensible pricing power as true value-add in Adobe’s case.

As one Photoshop Essentials review noted: “If you have an Adobe Creative Cloud subscription and need AI images for your project, the obvious choice is Adobe Firefly. A big advantage is that it’s included with Creative Cloud at no additional cost. Your other option is a third-party AI image generator, with Midjourney currently the most popular, but it requires its own monthly subscription.”

Long Term Market Conditions Favor Established Players

While equity and debt markets currently fund upstarts with distant revenue expectations, sentiment shifts can reverse this dynamic. Companies like Adobe with established distribution and stable subscription bases will be able to continue developing AI products while upstarts face funding pullbacks.

Third-Party Model Integration

Rather than competing with OpenAI and Midjourney, Adobe integrates these models directly into its products. This transforms potential competitors into assets that further lock users into Adobe’s ecosystem.

Adobe also recently announced a ChatGPT partnership allows ChatGPT users to access Photoshop, Express, and Acrobat within the ChatGPT interface. This is another new top of funnel, making sure photoshop users keep using photoshop even if they want to also use OpenAI products.

Image Generation Volume Data

As of September 2025, 15 billion images had been created from AI generators globally. Seven billion came from Firefly (Source). Even excluding third-party models integrated in Firefly, Adobe’s proprietary model generated 1 billion images versus 964 million for Midjourney and 900 million for DALL-E (Source).

That’s the power of distribution, before researching Adobe - I hadn’t heard of Firefly yet it is one of the more proliferent models out there.

AI-Influenced Revenue Tailwinds

Adobe is capturing AI revenue growth across multiple vectors simultaneously.

A. Upsell to Existing Enterprise Base

Adobe has stated that nearly 50% of Enterprise Term License Agreements upgraded to AI-enabled Acrobat Studio. Assuming enterprise Acrobat Pro pricing of $15 per seat per month versus Acrobat Studio’s $29.99 list price, represents a 100% price increase. Applied to 50% contract penetration, this generates a 50% revenue increase for the Acrobat product line. Adobe hasn’t broken down exactly which products this applies to, but it shows the pricing increase opportunity.

B. New Customer Acquisition

First-time Adobe subscribers originating from Firefly grew 30% in Q2 2025 and 20% in Q3 2025. While conversion rate data has not been disclosed, the trajectory indicates meaningful funnel development.

C. Net-New AI-First Revenue Streams

Management began reporting AI-first ARR (covering Firefly, Acrobat AI Assistant, and GenStudio) in Q1 2025 at $125 million. By Q3 2025, this figure surpassed the full-year FY25 target of $250 million, implying 133% full-year growth from Q1 to Q4.

Extrapolating this run rate, pure AI ARR reaches $1 billion by Year 2 (approximately $1.36 billion), representing 5% of total ARR assuming it keeps growing at 11%. That means AI revenues will already become a sizable chunk of revenues for Adobe within 2 years, and will likely only become more so.

Notably, management ceased reporting this metric after Q3 2025, likely due to the difficulty of separating “AI-first” from “AI-influenced” revenue as products became more integrated.

D. AI-Influenced ARR

AI-influenced ARR grew from $3.5 billion in FY2024 to approximately $8.4 billion exiting FY2025. Management stated this represents approximately one-third of the “book of business.” Assuming this ratio applies to total ARR of $25 billion yields us $8.4 billion AI-influenced, representing 140% year-over-year growth. That’s substantially higher than overall ARR growth.

Optionality: The GEO Market and SEMRush Acquisition

GEO refers to Generative AI Engine Optimization, or engineers business's digital asses to get favored by chatbots like ChatGPT and OpenAI. This is a brand new industry growing alongside the more established Search Engine Optimization (SEO).

Market Opportunity

Global SEO spend ranged from $65.87 billion to $89.10 billion in 2024 depending on reports.

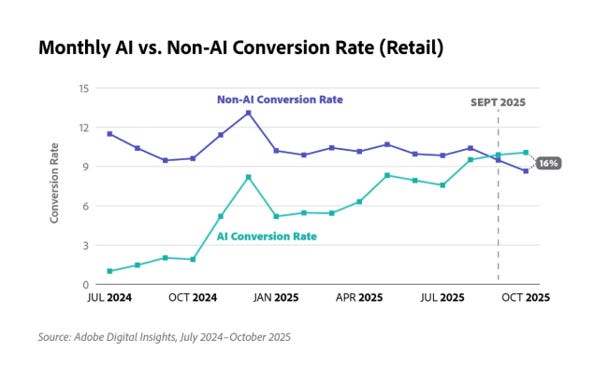

Bain research shows that 80% of search users rely on AI summaries 40% of the time. Napkin math implies that 32% of searches now occur through AI interfaces. Applied to the SEO market, this represents a $28 billion annual GEO opportunity that is growing rapidly.

As Bain noted: “Brands must evolve or risk losing visibility into their customer journey, and control over their brand positioning, in a world where traditional clicks are disappearing.”

McKinsey research suggests that up to 50% of brand traffic is at risk due to GEO, potentially impacting $750 billion of consumer spend.

We can safely assume that AI search will continue growing in important, we can make a safe assumption that GEO will become just as important to businesses as SEO, with the spend reaching comparable amounts. This is especially true as AI search retail conversion rates start matching traditional search:

Strategic Integration: Controlling the Full Marketing Funnel

The SEMRush acquisition allows Adobe to control three critical stages:

Content Generation through Creative Cloud

Distribution and Analytics through Experience Cloud

Optimization for AI Visibility through SEMRush and Adobe’s LLM Optimizer

Adobe recently announced an LLM Optimizer tool within Experience Cloud to tailor marketing assets to LLM crawlers. SEMRush, which has been an early pioneer of GEO analytics (along with competitor SimilarWeb) builds on Adobe’s LLM Optimizer strategy for AI-era brand visibility.

The acquisition provides optionality in a rapidly expanding market that Adobe is uniquely positioned to serve through its existing customer relationships and integrated product suite. I also believe that GEO still isn’t getting as much recognition as other areas of consumer AI. While people are trying to guess what the future of search looks like, its clear that AI will be a key part of it and so will GEO.

Comparables and Valuation

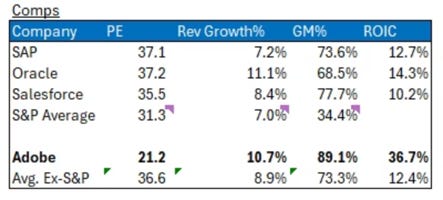

Adobe’s closest competitors among large legacy enterprise software providers are SAP, Oracle, and Salesforce. As we see above, Adobe has among the highest revenue growth, highest gross margin, and highest return on invested capital in this cohort. These key performance indicators have remained stable over three and five-year horizons.

Adobe also sports significantly better metrics than the S&P 500 average, yet trades well below it.

Despite the Company’s fundamental strengths, Adobe trades at 58% of its peers’ multiple.

Unlike other legacy enterprise competitors which primarily rely on AI for pricing uplift on existing products, Adobe has a tangible path to increasing paying user count by expanding freemium offerings at low marginal cost with brand-new AI-first products (Firefly).

Valuation Analysis

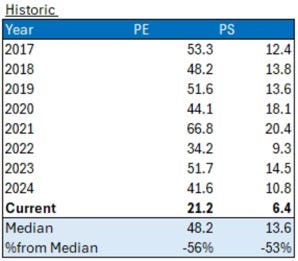

Adobe is trading at its lowest multiple in a decade and 56% below its median PE from 2017-2024.

Running a reverse DCF using company-guided operating margins and tax rate, a terminal growth rate of 3%, and a WACC of 9.58% (from Aswath Damodaran’s software industry estimate), the market is pricing in approximately 4% CAGR revenue growth over the next five years. This is despite the company guiding to 10% growth next year and all of its end-markets growing faster than 4%.

The fundamental question here is: Do you believe Adobe can clear a 4% revenue growth hurdle?

What multiple should ADBE command? Those historic PE ratios are associated with a period when Adobe revenue growth was higher and the company was enjoying the tailwind of converting its business to a subscription basis. A lower PE ratio is justified given slower growth. The question is how low the PE ratio should be.

I don’t think Adobe should command its historical median PE of 48.2 due to the slowdown in revenue growth. However, Adobe is a much higher quality company than the S&P average (31.3 PE) and the average of its peers (36.6 PE). Growth may be slowing, but Adobe has a strong route to ARPU expansion through generative tokens, freemium conversion, upsells, new pricing on AI products enabled by its distribution network, and disciplined margin control.

I hate doing valuation work because any one assumption changing will completely change the output. So lets start with a basic scenario, assuming no multiple expansion (remember, Adobe is trading at decade lows!).

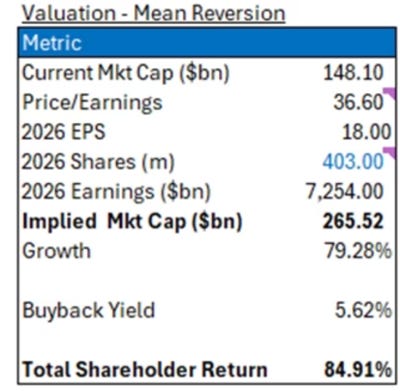

Base Case: 17% Total Return

Assuming steady-state multiples applied to Adobe’s 2026 guidance plus management’s guided buyback yield generates approximately 17% total return. This is all based on guidance, where management has historically been conservative, and announced buybacks, which management has also shown to be willing to be aggressive in.

Not bad for base case.

Now lets get optimistic and see what happens if ADBE reverts back to its peer group average (which in itself has contracted in the last couple of years).

Upside Case: 85% Total Return

Do I think this is what will happen? The truth is probably somewhere in between. Remember, the current price implies 4% revenue growth. If the market sees that ADBE is able to sustainably grow above that, multiples should expand.

Where will it land? Hard to say. Adobe could be one major product release away from catapulting itself to the forefront of the market’s mind. Perhaps next year the market starts focusing on the GEO opportunity and hones in on Adobe as one of the few ways to gain direct exposure to it.

How sure can we be that management matches or exceeds their revenue target?

From the Q4 2025 earnings call: “Q4 was a really strong quarter and frankly, starting to be this inflection in terms of, you know, as we see the leading indicators, what is happening across the leading indicators. You know, which gives us a lot of confidence. And that’s why, you know, when you look at the total Adobe AR growth target, you know, which translates to approximately 2.6 billion, that’s the highest beginning of the year guide for total net new AR.”

Adobe management is usually formal and conservative in their outlooks. To use the word inflection is pretty heavy language.

Risks and Mitigants

Enterprise Spending Slowdown

Adobe noted enterprise spending slowdown due to macro uncertainty. However, enterprise spending is cyclical and I would say already priced in. ADBE has been slumping continually since management made this comment.

GenAI Models Replace Photoshop

Current GenAI companies focus on image generation, not comprehensive editing. Adobe has integrated AI tools into their editing workflows. More importantly, enterprise customers remain wary of legal repercussions from using AI-generated images. Adobe’s indemnification and fully licensed dataset solves this pain point while competitors remain confined to the inspiration phase.

Vibe Coding Replaces Legacy Software

One explanation for SaaS multiple contraction is that AI-powered application builders could enable enterprises to create bespoke solutions. However, vibe coding currently suffers from quality issues with no built-in updates or customer service when systems break.

Enterprise reliability requirements make the cost/risk versus savings calculation unfavorable. As one developer noted at Where’s Your Ed At: “They frequently get weird and make strange errors, generally getting worse the further from ‘typical’ the work is. Because of the high error rate, I still have to read and verify every line, which is frequently much slower than writing them myself.”

Potential Risk: Freemium and the Top of Funnel

While Adobe’s freemium strategy shows promise, cheaper and free options like Canva represent genuine competitive pressure at the top of the funnel.

Competitive Context

Canva: approximately 220 million MAUs in 2025

Adobe (Firefly plus Express combined): 70 million MAUs by end of 2025

Midjourney: approximately 20 million registered members

Adobe’s Growth Metrics

Adobe’s freemium offerings are growing rapidly:

Firefly MAUs grew 30% quarter-over-quarter in Q2-Q3 2025

Paid Firefly subscriptions grew approximately 100% quarter-over-quarter in Q2 2025

Acrobat Web serves as an entry point for all PDF interaction needs and is growing 30% year-over-year

Student access (traditional customer pipeline) is growing 70% year-over-year

Product Parity Progress

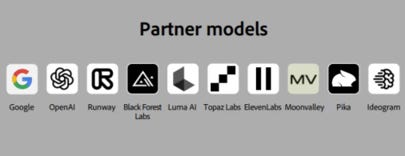

Adobe’s Firefly initially lagged rivals but has rapidly closed the quality gap according to TechRadar’s comparison. Additionally, their partnership strategy transforms the competitive dynamic. Adobe now houses OpenAI, Nano Banana, and Midjourney models within its ecosystem. Users access leading models without leaving Adobe’s environment.

The freemium model offers Firefly free with limited monthly Generative Credits, with upgrades to paid plans unlocking full access and serving as a gateway to professional offerings.

Conversion Funnel Indicators

Adobe now combines Express and Acrobat reporting, complicating direct comparisons. However, Express Organization wins growth has strongly outpaced MAU growth, implying successful conversion of trials to enterprise seats with improved monetization.

The risk remains that Canva’s significantly larger user base and aggressive feature development could capture would-be Adobe customers before they develop professional needs. However, Adobe’s strategy focuses on controlling the professional and enterprise segments where willingness to pay is highest, while using freemium offerings primarily as customer acquisition and brand awareness tools.

Microsoft Copilot provides a cautionary case study: as of August 2025, Microsoft had approximately 8 million active licensed users of Microsoft 365 Copilot. That’s a 1.81% conversion rate across 440 million Microsoft 365 subscribers, according to Where’s Your Ed At. However, Copilot became the second-most popular AI search engine, nearly tied with Google Gemini according to FirstPageSage. That is the power of distribution.

Several factors differentiate Adobe’s situation. Adobe operates a highly profitable non-AI-first business with over $20 billion revenue at 80% gross margins. AI features serve primarily as retention and ARPU expansion tools, not sole growth drivers. Adobe’s integration strategy (bundling AI into existing workflows) differs from the standalone product approach.

Conclusion

The market is pricing in 4% revenue growth over the next five years. The question is simple: can Adobe grow faster than 4%?

Given Adobe’s massive distribution and balance sheet, the structural tailwinds generative AI is providing the creative software segment , and multiple growth vectors withing Adobe’s product portfolio, the answer appears to be yes.

Thanks For Reading!

If you’ve found my work valuable, here are a few ways to support it, any help is greatly appreciated!

Subscribe to my Substack - just sign up below

Share feedback - let me know what I missed or could improve

Spread the word - pass this write-up along to friends or colleagues

Send me ideas - if I like them, I might write them up (win/win)

Pledge - If I start seeing a good amount of pledges, I may even do this full time!

Disclaimer: This article is for informational and educational purposes only. It is not investment advice or a recommendation to buy or sell any security. Please do your own research before making investment decisions.

I’ve always thought Adobe would be a beneficiary of AI, haven’t looked at their financials yet so I have no comments on that front.

Great to see such cogent analysis on Adobe.

Will have a read.